Will virtual reality conquer the Canadian mass market?

In 2017, high expectations for consumer adoption have given way to the realization that VR is still in its exploration phase. Pulse on VR presents an overview of the state of virtual reality in Canada in the first quarter of 2018.

For the VR industry, 2017 ended with mixed feelings, and the virtual reality (VR) industry is increasingly questioned by creators and storytellers. VR stakeholders are still searching for the killer app or the intuitive hardware that will drive adoption to the point where it achieves critical mass. Most notably, headset sales have generally been slower than expected.

The potential of virtual reality: some numbers from 2017

Despite this bracing reality, the global VR industry showed more signs for optimism in the second half of 2017, signalling that the potential of VR slowly but surely being realized, including:

- Global VR industry 2017 revenue amounted $6 billions , an 84% increase from 2016;

- Estimates of the number of VR head mounted displays (HMD) out there range from 9 to 15 million units;

- Sony PlayStation VR sales have exceeded expectations with more than 1.5 million units shipped in 2017;

- Location Based Entertainment acts as a consumer catalyst, introducing new audience to high-quality VR. In 2017, consumers spent about $800 million in VR arcades globally;

- Familiarity with VR continues to climb: 68% of US consumers have tried VR as of Q1 2018, against 67% last year;

- As hardware and software become more precise and professional, companies also start seeing commercial and educational use-cases (productivity tool, real estate virtual tour, tourism, etc.).

As for the headsets, although total sales did not reach the forecast figures, 2017 has been a record year for global headsets shipments:

A growing presence on the festival circuit

Content-wise, VR has grown to be recognized more and more as a medium of its own. Fiction and non-fiction VR content approach maturity as artists learn its own composition, acting and storytelling rules. Around the world, major festival embraced this emerging trend, including Canadian festivals:

- Cannes Film Festival: The Film Market dedicated 16,000 square feet to VR and new medias. Canada showcased 4 VR productions during two projections of its Canada Big on VR program;

- Berlinale: The European Film Market hosted the VR Now Summit to demonstrate how film, television and immersive media are all coming together. Stéphane Rituit, Co-founder of Montréal Felix & Paul Studios was the key speaker;

- SXSW Virtual Cinema: This year again, SXSW exhibited 25 projects ranging from 5 to 40 minutes;

- Sundance New Frontier: The festival’s selection presented more than 20 VR and AR projects;

- TIFF: The organization’s year long programming includes conferences and curated VR projects;

- HotDocs: North America’s largest documentary festival showcased ground-breaking VR projects in its 2018 DocX series.

State of the Canadian ecosystem

The industry has seen rapid growth in the last three years with 31% of VR products already in the market and generating revenue but is dealing with challenges such as limited financing (private and public) and the (im)maturity of the market. More than two-thirds of companies are developing content related products, and more than 86% of content products are interactive in nature. The industry is hopeful about VR becoming mainstream in four years.

Canada VR industry will continue to build on previous achievements in the coming year. With an estimated audience of 3.3 million Canadians, or less than 2% of the global VR audience, the Canadian VR industry will still manage to capture 3.5% of the total VR industry revenue in 2018.

Canada is particularly involved in the development of location-based VR entertainment. VR arcades and theatres are becoming one of the fastest growing sectors in this industry. Global spending in VR facilities is expected to double this year and Canadian players may already be positioned to capture this revenue. For example, CTRL V, one of the first VR arcade company, is now expanding in the US and counts 15 locations in North America with more to come. Vancouver start-up Mobile Reality brings VR to the people with the world’s first mobile VR arcade, launched in January.

Canadian VR content is also making a name for itself internationally. During its E3 conference, Ubisoft presented its VR title Transference, developed by its Montréal studio and coming next Fall, reaffirming the interest of major studios in VR games and the Canadian expertise in immersive entertainment. Short films by Felix and Paul Studios and are programmed in festivals worldwide.

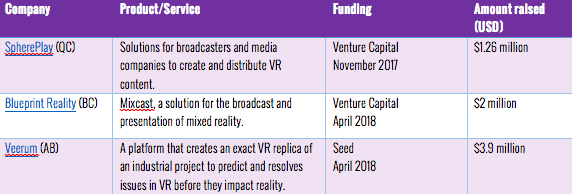

Investments in VR

Canadian companies continued to attract domestic and foreign investments in 2017. Interest in enterprise and vertical solutions increased in 2017, as shown by a select number of investments in Canadian companies outlined in the following table:

In addition to these successful fundraising rounds, an encouraging number of VR media projects have recently been funded through Canada Media Fund co-production programs:

- DNA Danse, a VR experience co-developed by Zone 3 (QC) and German studio INVR Space received over $120,000 in funding through the Canada-Germany Digital Media Incentive;

- 5 VR applications developed by Canadian and Israeli companies were granted about $775,000 in funding through the Canada-Jerusalem Co-development and Coproduction Incentive.

VR market forecasts

Global VR revenues are expected to grow by 91% this year, driven by head-mounted display (HMD) sales, VR cameras and location-based entertainment. The worldwide VR market will be valued at $11.5B as of year-end 2018.

Forecasts also indicate that almost 15 million head mounted displays will be shipped worldwide in 2018 (excluding Cardboard and similar basic products). The Canadian market will continue its steady growth and represent 2.6% of 2018 HDM shipments. Mobile-based headsets (e.g. Samsung Gear, Google Daydream View) are the most popular product.

Standalone headsets are a turning point in VR. They do not require connection to high-end expensive PC or consoles. In addition to the new Oculus Go and the upcoming Focus, Lenovo’s Mirage Solo and Pico’s Goblin are already on the market. Projections show that standalone headsets will be the fastest growing consumer HMD category in the next 5 years, playing a crucial role in the expansion of user base.

Launched at the end of June 2017, the bilingual website Pulse on VR presents an ongoing snapshot of the Canadian Virtual Reality (VR) ecosystem as it evolves. You will find in-depth case studies from some of Canada’s top VR players, a list of Canadian companies in this sector as well as information from jurisdictions across Canada.